This article appeared in the June 11, 2026 issue of the monthly print edition. Subscribe now.

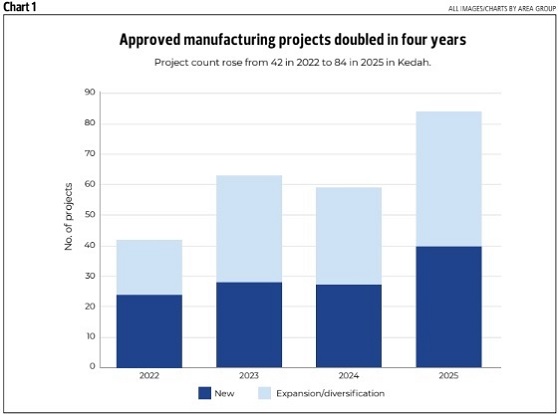

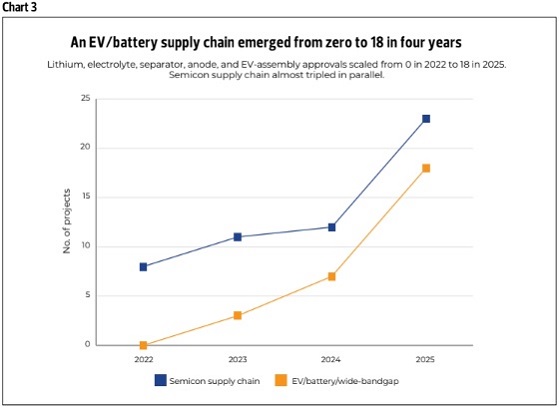

Malaysia’s northern corridor — comprising Perlis, Kedah, Penang, and Perak — is winning more industrial investment than at any point in its history. Kedah — the focus of this report — in particular has seen rapid growth over the last five years. Its Malaysian Investment Development Authority (Mida)-approved projects doubled over four years to 84 in 2025 (Chart 1), the fastest growth of any state, while EV approvals went from zero to 18 (Chart 3). Sungai Petani has emerged as Kedah’s fastest growing node, in terms of project count. Kedah’s high-value industry share matches Penang’s.

The China+1 reallocation is landing here for structural reasons — institutional familiarity, English‐language administration, an established intellectual property and customs regime, and a workforce the incumbent multinationals already know how to train — that Thailand and Vietnam cannot yet match.

The wider geopolitical environment is sharpening the urgency. Middle East tensions, shipping route fragility through the Red Sea and the Strait of Hormuz, and the broader reorganisation of global supply chains away from single-country concentration risk have all made manufacturers reconsider where they place new capacity.

The New Industrial Master Plan (NIMP) 2030 sets a target for less-developed states to lift their share of national manufacturing value-add from 22% to 30–35% by 2030. Whether Kedah delivers depends less on the headline foreign direct investment (FDI) announcements, than on whether the supporting ecosystem can be built quickly enough to convert strategic position into compounding tenant demand.

That is the question this report sets out to answer.

WHAT THE CURRENT INDUSTRIAL MAP ALREADY SHOWS

The northern corridor’s main clusters centre around Penang and Kedah. As mentioned, AREA Market Intelligence’s (AMI) analysis of Mida approvals shows Kedah’s project count rising from 42 in 2022 to 84 in 2025 (Chart 1), and Penang rising from 135 to 232. In comparison, Selangor grew from 265 to 410.

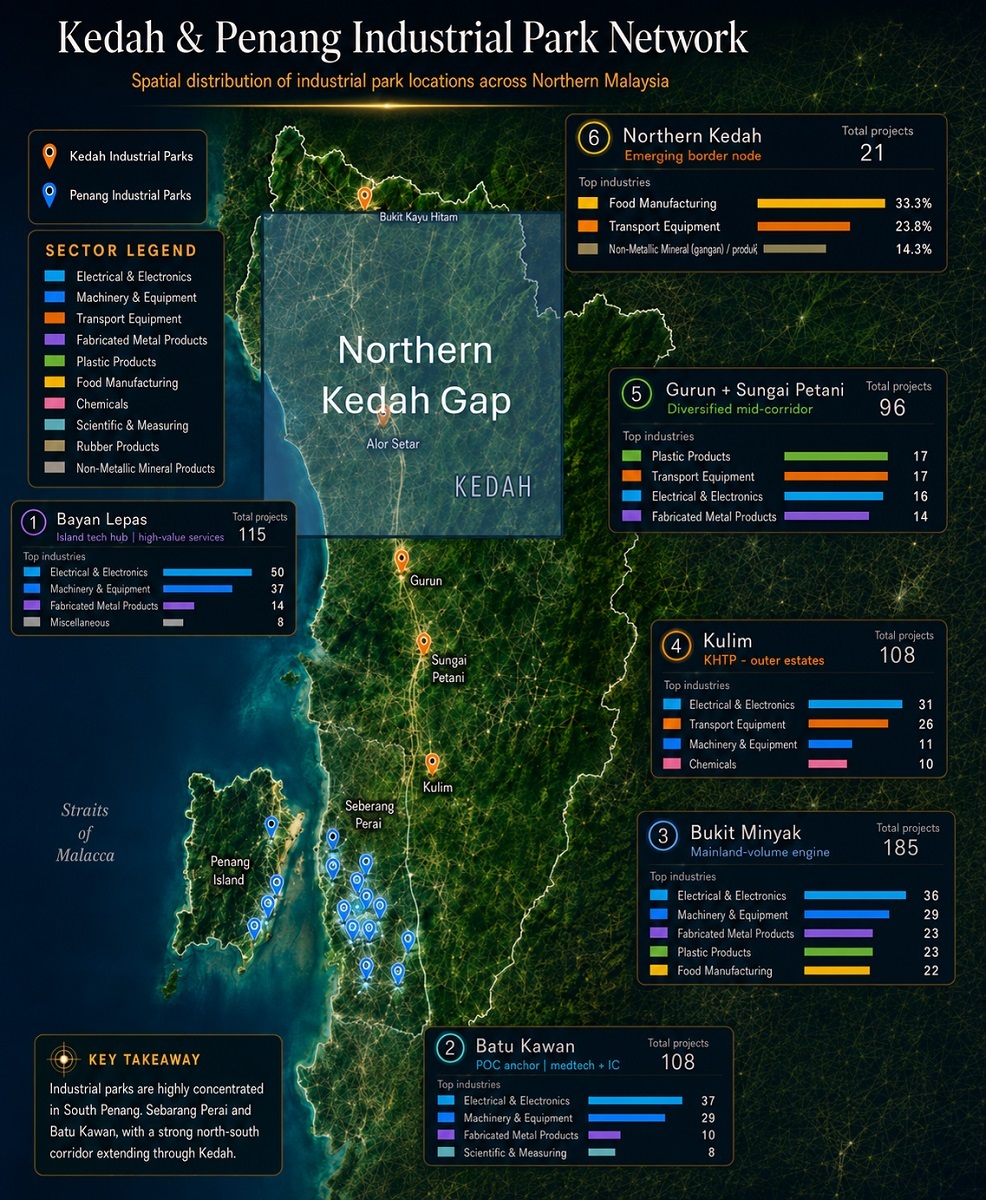

Kedah’s high‐value share rose from 38.1% to 63.1%; Penang’s from 46.7% to 63.4%. In Kedah, approvals cluster in Kulim, Sungai Petani and Gurun. In Penang, they remain anchored in Bukit Minyak, Perai/Seberang Jaya, Bayan Lepas, and Batu Kawan.

WHERE DEMAND IS MOVING NOW

Kulim, the demand‐led node

Kulim has the strongest demand narrative.

Kulim Hi-Tech Park (KHTP) Phase 3A practically sold out on launch day in 2024, mostly to EV‐ecosystem buyers rather than legacy electrical and electronics (E&E). KHTP is being absorbed by the industries the corridor is supposed to be diversifying into. With Phase 5 due shortly and contiguous land bank visibly running thin, the question now is whether the park can expand fast enough, or whether land in the surrounding Kulim and Sungai Petani estates can absorb the overflow.

Penang, the demand is settled; the supply is not

Batu Kawan remains the established centre of gravity in Penang, with US-based Lam Research’s new Batu Kawan facility being the latest layer on an already‐deep semicon cluster. Chatter points to a Batu Kawan Phase 2 expansion but nothing concrete has been announced. The harder question is no longer demand but supply. Mainland land is running thin, prices have roughly doubled in four years, and Phase 2, if it lands, is the only remaining lever to keep the pipeline in step with demand. Until then, the overflow logic points east.

Gurun and Sungai Petani, the quiet success story

What has changed over the last decade is the kind of industry the wider catchment attracts.

The historical heavy-industrial base continues to compound — Petronas Chemicals Group Bhd confirmed its long-term commitment with a 2023 melamine expansion, and Stellantis Gurun has used the site for its EV transition with consecutive 2023 and 2024 approvals. Shanghai Putailai’s 2025 graphite anode and carbon additive plant brings the EV battery supply chain directly to Gurun.

AMI counts approximately 100 approved projects across the combined Gurun and Sungai Petani catchment between 2022 and 2025 — close to Kulim’s 116 — spanning E&E suppliers, factory automation, precision plastics, and fabricated metal — a diversified mid-corridor backbone along the Asian Highway (AH)2.

Why Gurun? The land is cheaper than Kulim.

Gurun’s power station is undergoing major capacity upgrades, with the grid and water supply being scaled ahead of demand. Housing supply is ample. And the AH2 gives both nodes seamless access to Penang Port and Bayan Lepas, letting operators and their workforce move across the corridor seamlessly. Infrastructure is built in parallel with industrial demand rather than after it.

WHAT THE TRANSACTION DATA SHOWS

An analysis of industrial transactions over 2022– 2026 shows a clear pricing hierarchy across the wider northern region. At the top sits Penang’s mainland, where built-up factory transactions have moved from a median of RM604 psf in 2022 to RM1,288 in 2025. Penang is no longer cheap relative to its own history, with the fouryear period median around RM818 psf reflecting a market that has structurally re-rated as Bayan Lepas and Batu Kawan absorbed the semiconductor and E&E wave. The mainland land bank is running thin and the pricing reflects the constraint.

Inside Kedah, the pricing tells the narrative of two different industrial geographies. Kulim and Sungai Petani both transact in the RM285– RM289 psf range, pricing as genuine peer nodes despite their different historical positioning. Kulim is the established federal park; Sungai Petani is the emerging node. The fact that they now trade at near-identical prices is itself analytically significant — indicating the market is treating the mid-corridor catchment as a single industrial geography rather than as two separate locations.

For reference, Selangor sits between Penang’s premium and Kedah’s emerging mid-tier. Kuala Langat transacts at around RM473 psf and Klang at RM397 psf, both reflecting the Klang Valley’s logistics premium and its proximity to Port Klang. These are not Penang-equivalent prices, but they are meaningfully above the Kedah catchment.

Alor Setar runs at roughly half the Kulim and Sungai Petani level, at around RM137 psf.

The state capital is not yet absorbing industrial demand the way the mid-corridor is. Vacant industrial land across the wider Kedah corridor ranges RM29–RM35 psf, which is the baseline against which any future industrial development will be priced.

The thinner sample at Kubang Pasu tells a different story entirely. Median vacant industrial land has moved from RM12 psf in 2022 to RM29 in 2024. A 28-acre parcel on the road to the Thai border was acquired in late 2023 at RM18 and resold in three lots a year later at RM29 across all three.

The pattern

The pricing arc tells a coherent story. Penang’s mainland has re-rated structurally as the semiconductor cluster matured and the land bank tightened. Selangor remains the logistics-premium alternative for occupiers who do not need to be in the north. Kulim and Sungai Petani have established themselves as peer nodes in the mid-corridor and the market is treating them accordingly. Alor Setar is not yet part of that re-rating. And the Kubang Pasu pricing is running ahead of the tenant demand that would normally underpin a price move, most likely driven by the Bukit Kayu Hitam Special Border Economic Zone (SBEZ) announcement rather than by industrial fundamentals.

Kedah State Economic Planning Unit director Junaidi Abdul Rani, Ministry of Finance Government Investment Companies Division undersecretary Datuk Amiruddin Muhamed, AREA Group executive chairman Datuk Stewart LaBrooy, Northern Gateway (NGX) group CEO Razwin Sulairee Hasnan Termizi, NGX chairman Datuk Zamzuri Abdul Aziz, Shenzhen Government Procurement Association chairman Feng Qiang, Malaysian representative of China Development Institute Chim Teng Lee, and Zonghebang Digital Consulting Co Ltd chairman Ma Xu Guang at the bilateral cooperation signing ceremony of the China-Malaysia ‘Two Countries, Twin Parks’ initiative aimed at developing 1,500 acres of industrial land at Pentas Industrial City (Pentas) within the Delapan Special Border Economic Zone (SBEZ) ecosystem in Kedah")

The central spine has earned its repricing.

The Kedah catchment around Kulim and Sungai Petani is now seen as a genuine alternative to Penang’s mainland rather than as a discount play. The border plays have not yet earned their repricing on tenant demand alone. What separates the two is the subject of the next section.

The arbitrage between Penang’s mainland and Kedah catchments has roughly tripled since 2022 and continues to widen.

FROM SPILLOVER TO ECOSYSTEMS

The central spine works because the surrounding conditions were built in step with industrial demand. Kulim has the federal park designation, the Penang Port and Bayan Lepas access via the AH2, the established multinational tenants that anchor the supplier ecosystem, and a state government that has spent administrative and political capital to land each new commitment. Sungai Petani and Gurun have absorbed the spillover because the land was cheaper, the road access was comparable, the housing supply was ample, and the infrastructure was being built ahead of tenants rather than after them. These are not accidents. They are the result of deliberate, parallel build-out across the conditions that determine whether industrial activity can compound.

The parts of Kedah that have not yet compounded share a common pattern. Projects are sold as land stories, with the keyword being “spillover” (the NIMP even states it). More often, the anchor lands in a thin environment.

Approvals stay fragmented. Worker housing arrives late. Schools and healthcare lag. Supplier depth takes years longer than the investment deck promises. Too many master developers run the same playbook: keep land lightly improved, market it as catalyst‐ready, and wait for the single transformational tenant. That is not a development strategy. It is a passive option position on someone else’s decision.

If Kedah wants to move beyond the spillover narrative, it needs to stop asking only “how much land is available?” and start asking:

*Can people live there?

*Can companies find workers there?

*Can suppliers operate there?

*Can goods move efficiently from there?

*Can power, water, and fibre be delivered when needed?

*Can approvals be managed without exhausting the investor before operations begin?

Underneath all six is the harder question: what is the area’s actual value-add? What can this site offer that no other site can? Spillover, on its own, is hit-and-hope. Value-add provides the gravitational pull.

THE NORTHERN BORDER BELT

Beyond Sungai Petani and Gurun lies a 100km stretch of largely rural Kedah and Perlis, for which AMI has coined the phrase the “northern Kedah gap” (Map 1), that the Northern Corridor Economic Region (NCER) has bet on as the next industrial frontier.

Three major projects are currently active along the Perlis, Kedah and Thailand borders.

Chuping Tech Valley, Kedah Rubber City (KRC), and Bukit Kayu Hitam (BKH) (comprising the Delapan SBEZ and Kedah Science and Technology Park).

Each has been positioned as the next industrial frontier. Each carries a defensible thesis about why it could compound. None has yet built the surrounding ecosystem that would convert the thesis into compounding tenant demand. This section examines each one against the value-add framework, what the site offers that no other site can, what the constraint is, and what the path forward looks like.

Delapan SBEZ

Delapan is a 4,000-acre, federally designated industrial, commercial and residential node with Northern Gateway Sdn Bhd, a subsidiary of the Ministry of Finance, as master developer.

It is the formal expression of NCER’s ambition.

Its goal is to deliver three things at once: capture cross-border trade, absorb adjacent Thai-side activity, and serve as a new hub in the northern industrialisation narrative. Each is plausible.

Stacking three on one site is a tall order, particularly because the northern SBEZ faces southern Thailand, a manufacturing economy with a broadly similar labour-cost profile to Malaysia’s. Cross-border zones succeed when there is a real reason for goods to stop and be processed before crossing the border. Shenzhen and Hong Kong work precisely on that logic. The Johor–Singapore Special Economic Zone works on the same principle.

Delapan’s value-add rests on three advantages: the federal SBEZ designation and its framework benefits, the single most active land-trade crossing between Malaysia and Thailand with working freight flows already moving through it daily, and proximity to the largest concentration of submarine cable landing stations outside Singapore at Satun and Songkhla. Federal incentives, working overland trade and submarine cable proximity are the analytical recipe for a digital and logistics ecosystem the Klang Valley and Johor clusters cannot replicate.

The private sector is moving. Local and foreign players have committed over RM20 billion in announced investment, anchored by PKT Logistics Group Sdn Bhd–Northern Gateway inland container depot, which is fully operational.

The trajectory will depend on whether matching public investment in utilities and access infrastructure arrive in step.

Kedah Rubber City (KRC)

The 1,244‐acre KRC opened in 2020 at Padang Terap, 58km from the AH2 turnoff. KRC’s value-add is genuinely specific: it sits within an established Malaysian rubber processing ecosystem, with proximity to natural rubber inputs from northern peninsular Malaysia and Thailand, and with the institutional infrastructure for rubber-grade certification that the country has built since the 1970s. The current material anchor is Prinx Chengshan’s RM2.6 billion tyre investment. Plot pricing of RM22–RM35 psf signals what the state already knows: this will work as a downstream rubber and specialty chemicals cluster, or not at all.

Chuping Valley

Chuping Valley in Perlis sits further west still, off the AH2 spine. Its 2,482 acres are the largest paper-play in the northern belt with the thinnest confirmed demand. However, the supporting theses hold up. Perlis has among the highest solar irradiance levels in peninsular Malaysia, and Universiti Malaysia Perlis produces engineering graduates whose skills map directly onto E&E recruitment needs in Penang, Kulim and Selangor. The defensible play sequences the assets rather than marketing them in isolation: utility-scale solar generation first, anchoring a downstream low-carbon building materials cluster drawing on the local resources, and rail-served regional distribution.

The common challenge

The three sites have genuine value-add. The central spine has shown what is possible when industrial demand and supporting infrastructure develop together. The same principle applies across the corridor. The sites that combine value-add with a fully-developed ecosystem, housing, utilities, schools, supplier depth, connectivity, the soft and hard urban services that make an industrial address a place where people choose to live and work — are the ones that build into working industrial regions over time.

The border-play sites are well positioned. Each carries a distinctive value-add that no other site in the corridor can replicate. The combination of private sector commitment, federal designation, and state government engagement is the foundation on which the next decade can be built.

NIMP 2030: WHAT THE DATA DOES, AND DOES NOT, SUPPORT

NIMP 2030 has remarkably little to say about the northern corridor by name. The closest the plan comes to a place‐based agenda for Kedah and Perlis is an “E&E and M&E (mechanical and engineering) cluster spillover” arrow on its nationwide cluster map (Map 2).

The framework rests on six measurable targets, as summarised in Infographic 1. The target that matters most for Kedah is the fourth — lifting less-developed states from 22% to 30–35% of the national total by 2030. Kedah’s three-year track record supports the direction.

But Selangor’s pace makes the target challenging. The wage target is the genuine outlier, as no seven-year window in Malaysian manufacturing history has delivered 9.6% nominal wage growth without an external shock.

WHAT THE WORLD ALLOWS

NIMP 2030 was written for a global environment that no longer fully exists.

The first is the Strait of Hormuz and the wider Middle East shipping route fragility. A sustained Hormuz disruption would push energy prices sharply higher, with knock-on effects on Malaysia as a whole.

The second is US–China relations and the Trump administration’s reinforcement of decoupling. The China+1 reallocation is itself a function of US-China tensions. If those tensions ease, the reallocation flow weakens. If they intensify, Malaysia faces pressure to align more explicitly with one side, which would constrain the multi-aligned investor base the corridor currently enjoys. NIMP 2030’s hightech export doubling depends on continued US market access on terms broadly similar to today’s. That access is not guaranteed.

THE HONEST POSITION

The direction of NIMP 2030 is broadly supported by what Kedah is showing on the ground: project counts, high-value share, EV battery emergence. But the numerical targets are mixed, and the external environment may make even directional progress harder than the plan anticipates.

The most useful thing Kedah can do over the next seven years is to keep over-delivering on the direction, build the supporting ecosystem that gives the corridor durability against external shocks, and accept that the headline targets may need to be revisited if the operating environment continues to deteriorate.

CONCLUSION

Kedah is closer to becoming one of Malaysia’s most important industrial growth stories than at any point in the last forty years.

The evidence is on the ground, not in the brochure. Project counts are up, and the quality of approved investment has shifted. EV and battery, wide-bandgap semiconductors, chemicals, precision manufacturing, and the E&E activity that feeds them are beginning to reshape the corridor. Sungai Petani and Gurun are no longer waiting rooms for activity drifting north from Penang. They are becoming genuine peers to Kulim inside a wider mid-corridor geography.

But Kedah cannot afford to mistake spillover for strategy.

Made in China 2025 taught the rest of the world a blunt lesson: industrial advantage is built, not received. China did not wait for advanced manufacturing to turn up. It assembled the ecosystem to accommodate it and the coordination to develop both in parallel.

China+1 is the world’s reaction to that success, and to the concentration risk it created.

As companies diversify their production base, Malaysia has a real chance to capture demand it did not have to manufacture.

But good things don’t often happen by accident. If we take in relocated factories without building the stack beneath them, we don’t become an industrial node. We become a back room in someone else’s system. The plant sits here, but the machinery, the components, the software, the supplier depth, and the decisions that carry the margin stay somewhere else. We would hold the activity and forfeit the value.

That is the work of ecosystem building.

Building functioning industrial communities – scalable utilities, dependable network connectivity, worker housing, schools, healthcare, and technical and vocational education and training (TVET) that make an address liveable, supplier networks that deepen, and customs and approvals that move at the speed of capital. Get that wrong and the symptoms are predictable. Land prices running ahead of fundamentals, factories without local suppliers, workers who commute instead of settle, and border zones that stay policy ambitions rather than working regions.

For Kedah, and for Malaysia, it stops being merely a real estate question. It becomes a question of whether we own a layer of the next manufacturing era or merely host it. We can wait for factories to fall out of China+1 as a by-product, or we can build the ecosystems that capture the higher-value share, deepen domestic capability, and earn Malaysia a durable seat in global manufacturing.

This is especially important for the northern border belt. Delapan SBEZ, Kedah Rubber City, and Chuping Valley each have a defensible value-add. But value-add only becomes economic gravity when the ecosystem around it is deliberately built.

For Kedah, and for Malaysia, this is no longer only a real estate question. It is a nation-building question.

Alistair LaBrooy is director at the AREA Group of Companies, a real estate advisory, market intelligence, and development group, with capabilities in real estate investment trust (REIT) and investment management services.

..........

Read about emerging trends, data-backed insights, growing subsectors, and expert commentaries in EdgeProp print. Subscribe now for your free copy!

{kind=link}