")

KUALA LUMPUR (March 13): The Real Estate and Housing Developers' Association (Rehda) said over two-thirds of prospective homebuyers in Malaysia fail to obtain financing for property purchases, mainly due to high debt obligations and inadequate income levels.

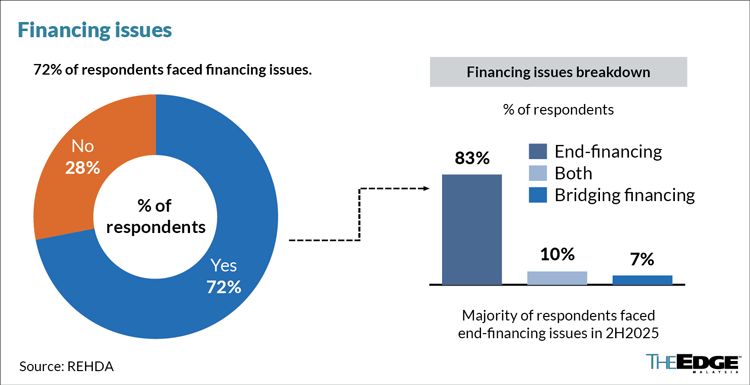

A survey by the property agency involving 166 developers found that 72% of respondents encountered financing-related difficulties among buyers, with most citing bank rejections of end-financing loans as the primary obstacle.

End-financing — mortgage loans provided by banks after a purchase agreement is signed — enables buyers to complete transactions, while other cited challenges that included issues with bridging financing or a combination of both.

“If buyers have outstanding credit card balances or excessive debt commitments, it affects their eligibility for housing loans,” Rehda president Datuk Ho Hon Sang told reporters during the association’s latest Property Industry Survey briefing.

Many applications were rejected by the banks due to insufficient income levels, high credit card commitments and incomplete financial documentation submitted by buyers, Ho noted.

“Many times, we encourage developers to guide buyers on managing their finances, but ultimately, if they do not meet the eligibility requirements, it becomes difficult for banks to approve the loan,” he added.

The financing challenges come at a time when Malaysia continues to face a structural mismatch between housing prices and household incomes.

Previous research by Khazanah Research Institute found that households earning below RM3,000 per month account for about 15% of Malaysia’s population, yet only around 3% of the new housing supply is affordable for this income group.

Although roughly half of new housing launches are priced below RM300,000, they are still beyond the reach for many lower-income households.

In its survey, Rehda found that homes priced between RM500,001 and RM700,000 recorded the highest mortgage rejection rates, with 31% to 45% of transactions failing to obtain financing approval.

The findings also suggest that affordability pressures are not confined to lower-income groups but are increasingly affecting Malaysia’s middle-income households, traditionally seen as the core segment of the residential property market.

Rehda's immediate past president, Datuk NK Tong, added that the gap between income growth and property prices remains the underlying driver of financing difficulties.

“As a thought experiment, if developers are required to cross-subsidise housing, should we not also consider something similar for home loans?” he said.

“Perhaps banks could allocate about 30% of their mortgage portfolios to affordable housing loans. If that happens, they will also work harder to accommodate borrowers who genuinely need assistance.”

Such proposals, he added, could help narrow the gap between housing supply and homeownership accessibility, particularly for lower- and middle-income Malaysians.

Bridging-financing issues

Rehda also noted that financing conditions have become increasingly stringent, affecting not only homebuyers but also property developers themselves.

Bridging finance, which means short-term funding used by developers during construction, has also become harder to secure, with banks requesting additional documentation and imposing stricter drawdown conditions.

Some banks now require developers to achieve sales thresholds of between 30% and 60% before releasing financing, adding to project funding pressures, the association noted.

Notably, unsold housing inventory has risen across Malaysia.

As of end-2025, 60% of developers surveyed reported unsold completed residential units, with loan rejections, weak demand and high property prices cited as the main reasons.

By price range, 47% of unsold units were priced below RM500,000, while 23% was priced above RM1 million.

In terms of property types, two- to three-storey terrace houses accounted for 26% of unsold units, followed by serviced residences (19%) and single-storey terrace houses (18%).

“Even single-storey houses are no longer selling like hot cakes,” Ho said.

“But it also depends on location and the specific market where the project is launched.”

However, Ho noted that the survey figures do not reflect the exact number or geographic distribution of unsold units, as conditions vary significantly across states and local markets.

..........

EdgeProp's inaugural monthly print edition is fresh off the press! Free delivery is available for selected regions. Subscribe now.

.png?sNjuasipxlg5fTSjsjME58JKmvF7nf2I)

{kind=link}