This article appeared in the March 12, 2026 issue of the monthly print edition. Subscribe now.

Malaysia’s industrial property market has moved beyond the “land + brochure” era.

Outperforming assets are no longer just well-priced plots inside a boundary line; they are locations that behave like reliable operating platforms. End-users are looking for uptime, dependable utilities, predictable travel times, a reliable workforce, and approvals that do not derail global rollout schedules.

The change is visible in how serious operators screen sites. The questions are consistent:

*Can we run? (power, water, network, resilience, expansion pathways, key utilities delivery speed)

*Can we hire? (labour catchment, commuting reality, retention, skills pipeline)

*Can we move goods and people? (route reliability, congestion, security, gateway access) Only after these questions are answered do incentives and land pricing come into play.

These operators’ seal of approval, demonstrated by their investment, typically drives further spending in the area. As suppliers converge and infrastructure deepens in response to proof of demand, momentum builds, and an area is gradually transformed into an industrial cluster — as demonstrated in Penang and Selangor.

When industrial properties are built without considering these factors, two things may happen. In the first scenario, they may still “sell” on paper, but take-up ultimately stalls at the end-user level. “For Sale/To Let” boards, frequent tenant churn, and clusters that take longer to develop day-to-day operating density point to this.

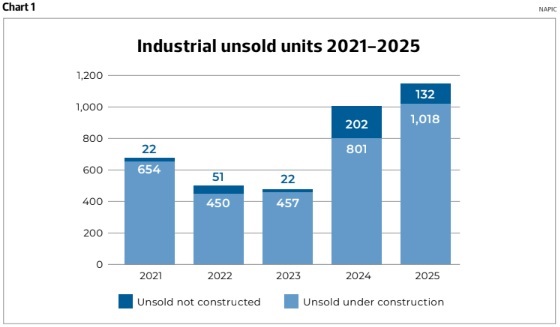

In the second scenario, unsold stock accumulates. National Property Information Centre (Napic) data show that between 2022 and 2025, unsold units under construction climbed from just 22 to over 1,000; a 45-fold increase in four years (Chart 1). That indicates a pipeline is being built ahead of proven demand.

One reason behind this is speculative development that mistakes proximity to a hot zone for a viable site thesis. When demand concentrates in a proven node, the instinct is to spill supply into adjacent areas, but spillover is not site selection.

The roads, utilities and logistics networks that made the original node work have been sized for that node, and do not automatically stretch to serve a new one.

What happens next is predictable: approvals slow, utility connections lag, and tenants who expect the same operating conditions find a different reality on the ground.

The deeper problem is that speculative supply often starts from land availability and price arbitrage, and the assumption that what has worked nearby will work here. Without proper market research into what tenants actually need; power specifications, water volumes, workforce catchment, route reliability — a site that looks viable on a map becomes a liability in operation.

Delivery beats declarations

As competition among our regional peers grows stiffer, we must prove we can add more value to the strategic industries needed to transform our economy. The answer is not a single lever — it is two that must move together.

Governments must go beyond administrating. It must upgrade roads and interchanges, expand ports and airports, strengthen utilities and reserve margins, improve security and route reliability, and coordinate delivery sequencing across agencies. In other words, move away from facilitating, towards platform-building.

But platform-building works faster and costs less when it is focused on the right ground.

That is where strong site selection comes in — identifying locations already ripe for development, where older industrial belts have proven the fundamentals, and where the next wave of growth can compound on what already works rather than starting from scratch. One example is the Dengkil Corridor in Sepang, Selangor.

Utilising the underutilised

The Dengkil Corridor traces a continuous industrial spine running from Carey Island in the west, along the SKVE through Banting, and terminating at Dengkil in the north. The corridor has been taking shape organically along an established highway alignment, with industrial activity already anchored at multiple points along its length. The question is no longer whether it exists, but whether it will be developed with the discipline its fundamentals deserve.

Dengkil’s proposition is compelling because much of the corridor thesis is already grounded in measurable fundamentals, and it sits inside an explicit state platform.

The Selangor First Plan (RS-1) frames the Integrated Development Region in South Selangor (IDRISS) as a consolidated development push across South Selangor (Sepang and Kuala Langat), signalling coordination rather than piecemeal projects.

The private market signal is growing clearer: in January 2026, IOI Properties Group Bhd announced the disposal of 136 acres at IOI Industrial Park @ Banting to Bridge Data Centres for RM740.68 million, or around RM115 to RM137 psf (based on media reports). This is the kind of flagship transaction that typically accelerates follow-on attention because it implies serious diligence has already been performed.

The corridor logic is straightforward (Map 1):

*Close enough to compete for tenants within the Klang Valley’s employment and supplier hubs

*Far enough to offer physical runway for phased growth outside saturated nodes

*Connected enough to function as a practical gateway matrix for logistics and digital infrastructure

*Ample blue and white collar workforce through surrounding mature and upcoming housing estates

*Ample scalable utilities

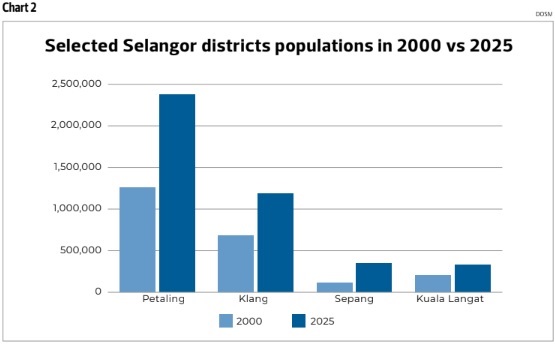

The demographics are not theoretical: South Selangor has real runway

The district growth story supports the corridor thesis: South Selangor’s growth includes population, households, and residences, which matter because labour catchments are built from housing and commute realities.

In 2025 preliminary estimates, the Department of Statistics Malaysia (DOSM) reports Sepang’s population at 350,400, and Kuala Langat’s at 329,000; both are meaningfully larger than their 2000 baselines (Chart 2).

Connectivity that supports the corridor thesis

Dengkil’s access to the West Coast Expressway (WCE), South Klang Valley Expressway (SKVE), and North-South Expressway Central Link (ELITE) highways matters because it improves route options: quicker access into the Klang Valley, practical bypasses, and cleaner linkage into the north–south movement of goods (including Penang connectivity via the PLUS system, where WCE ties into the national highway network).

The WCE itself is positioned as a coastal relief corridor running from Banting towards Taiping, Perak, designed to link with key existing expressways (Map 3).

A single ‘utilities assessment’ for Dengkil

Power: grid build that can be proven

Data-centre-grade and advanced industrial users do not buy promises on power. They buy connection pathways, reinforcement visibility, and timelines.

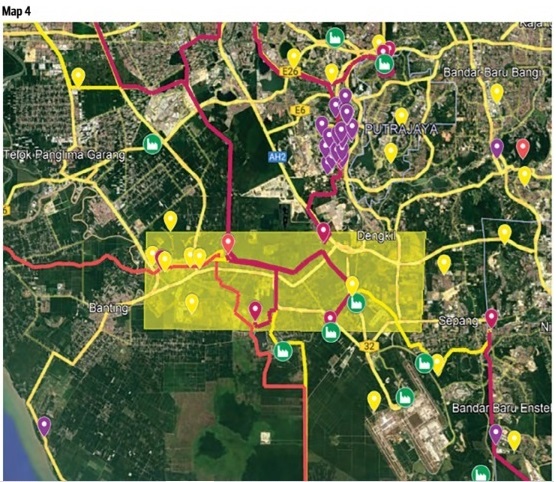

Dengkil has credible pathways via a reinforced southern grid context. One tangible signal in the broader southern Selangor system is the Pulau Indah Power Plant (1,200MW), which achieved commercial operation on March 1, 2025, under a 21-year agreement structure, according to reports (Map 4).

For corridor messaging, the takeaway is simple: investors can perform due diligence “hard assets” (generation, transmission strengthening, substations, and intake options) far more easily than they can diligence vague upgrade promises.

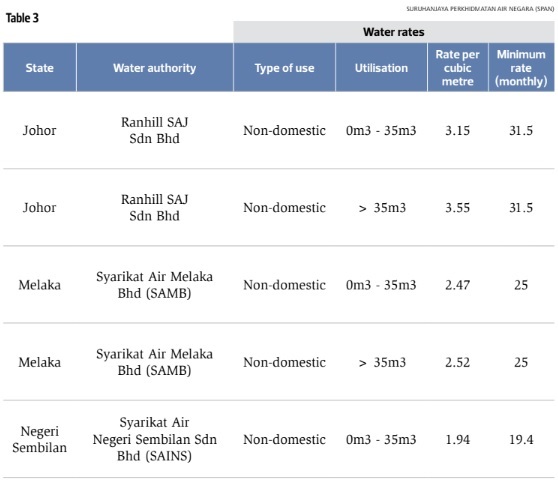

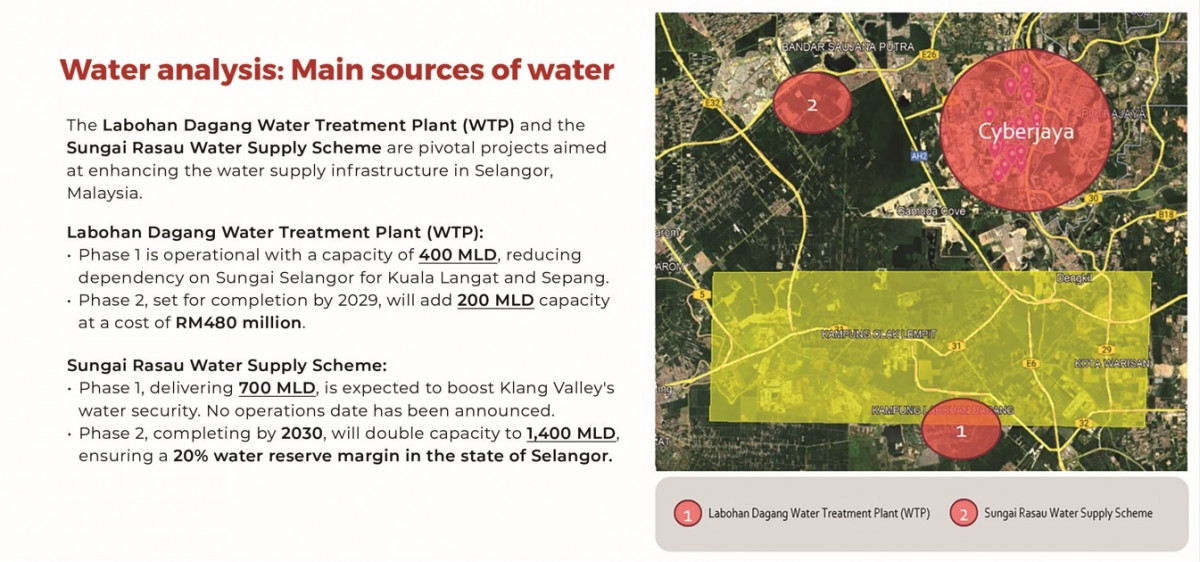

Water: capacity expansion and industrial-grade alternatives

For industrial and data-centre-adjacent uses, water is increasingly treated like power: a utility that must be planned at corridor scale.

Selangor’s medium/long-term capacity projects (including the Sungai Rasau Water Supply Scheme and subsequent build-outs) matter because they increase reserve margin and resilience across the broader system that supports South Selangor’s growth spine (Map 5).

On pricing signals: Malaysia is heading towards premium tariffs for resource-intensive users. Reports have referenced a special tariff for data centres in Selangor (e.g., RM5.31/ m3 in one cited discussion), reinforcing the point that utilities are becoming more explicitly “cost” for hyperscale demand.

For environment, social, and governance (ESG) positioning, reclaimed/non-potable industrial supply options also matter because they reduce pressure on potable allocations while strengthening sustainability narratives (and, most importantly, approvals).

Map 5

Proposed special water tariff for data centres

A new rate of RM5.50 per m3 is being established specifically for data centres, reflecting their high water usage, and ensuring infrastructure cost recovery. This is part of a broader government initiative requiring hyperscale or resource-intensive facilities to pay a premium for both water and energy.

Cyberjaya adjacency and highway-aligned routes make Dengkil ‘placeable’

For data centres, the network is the third utility. Power and water alone won’t cut it without diverse fibre paths, and credible interconnection options.

Dengkil’s advantage is twofold:

1. Cyberjaya adjacency (Malaysia’s most established interconnection ecosystem) supports practical backhaul and peering/onramp access. DE-CIX (Deutsche Commercial Internet Exchange) has expanded services in Cyberjaya (including activity tied to an NTT DATA campus), reinforcing Cyberjaya’s role as a major digital connectivity hub.

2. Highway-aligned corridors (WCE, SKVE,ELITE) often make fibre placement and route diversity easier because rights-ofway and maintenance access are simpler.

In corridor terms, power and water make Dengkil viable; network corridors make it placeable.

What to protect as Dengkil scales: making the corridor ‘priceable’

Dengkil’s fundamentals are already bankable.

The execution risk now lies in whether those ingredients are converted into a repeatable corridor product, something institutional investors and global tenants can price with confidence.

Start delivering ecosystems with the right products

Malaysia’s next phase of industrial growth will be driven by those who deliver a working, investable ecosystem that attracts value-add industries, with developers, site-selection specialists, industry experts, and government aligning planning, infrastructure, and approvals into one executable plan.

That is the real lesson from Penang and Shah Alam: clusters form when the operating system works, when the first anchor proves the platform, and when follow-on investors can move quickly because the fundamentals are visible.

IDRISS gives Dengkil the institutional spine, and South Selangor’s gateway and utilities trajectory gives it physical credibility. The task is now simple to define, but hard to deliver: make capacity transparent, make approvals time-certain, and phase supply against absorption.

If that discipline holds, the Dengkil Corridor won’t need hype. It becomes a repeatable platform, where industrial users, logistics operators, and digital infrastructure can scale with less risk, faster timelines, and better economics.

And that’s how industrial property stops being a speculative asset class, and returns to its proper role: productive infrastructure that compounds national wealth.

..........

Alistair LaBrooy is Director at the AREA Group of Companies, a real estate advisory, market intelligence, and development group, with capabilities in REIT and investment management services.

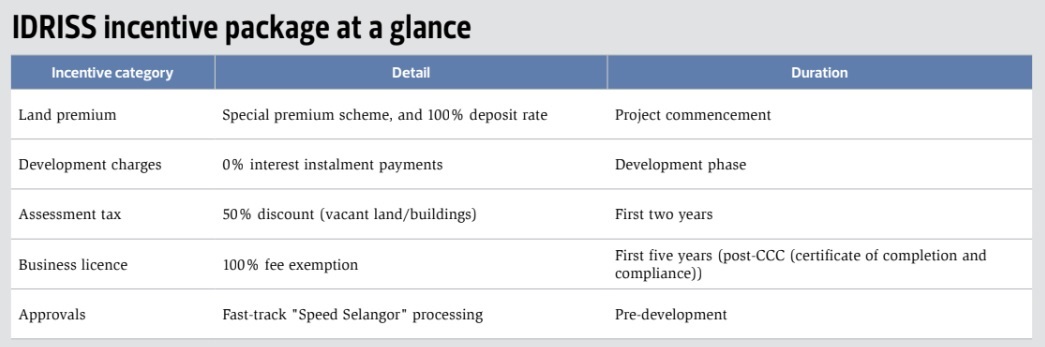

THE POLICY PLATFORM IS EXPLICIT, NOT VAGUE

RS‐1 describes IDRISS as an integrated private investment development in Sepang and Kuala Langat, driven by the state government and backed by state and federal incentives, with a stated 40,000-acre footprint, and headline gross-development-value valuation. It also names governance mechanisms (task force facilitation, and the Selangor Golden Triangle committee role) and lists priority projects inside the South Selangor spine.

On the ground, the state has been explicit about speeding approvals. Reports frame the Speed Selangor initiative as a catalyst to streamline processes for businesses and investment projects, exactly the kind of “timerisk reduction” that tenants and institutional capital value.

Here’s what governments can do to build industrial ecosystems:

1. Make capacity legible, and share it openly

The single highest-leverage move is transparent utility corridor data-sharing that includes:

*power capacity roadmaps (MW, intake options, reinforcement sequencing)

*water supply roadmaps (allocations, reserve margin direction, timeline certainty)

*network placement corridors, and diversity options

*standardised requirements, and hand-offs between agencies/utilities

The more a tenant knows, the faster they decide. The less they know, the more likely they are to pause or walk away. National competitiveness cannot be decided in departmental silos.

2. Treat ‘time certainty’ as infrastructure

For modern logistics and mission-critical projects, delays are costly. If approvals are required at the federal level (and utilities won’t advance feasibility until upstream approvals are secured), then the corridor’s competitive edge comes from making the pathway predictable: published timelines, clear requirements, and clean sequencing.

3. Phase supply against absorption, not optimism

The aim is to scale at the pace end-user absorption, utilities readiness, and approvals throughout allow, so growth compounds rather than stalls. This also means approving projects that can deliver clear economic and social benefits, not ones that merely cater for speculators. One way to gauge this is to have developers deliver clear mandates from clients to deliver operations in a given area.

..........

EdgeProp's inaugural monthly print edition is fresh off the press! Free delivery is available for selected regions. Subscribe now.

{kind=link}