This article first appeared in the Industrial Special Report in November 2025.

Functioning as a social enterprise, and as an independent training, research, and education arm, the Real Estate and Housing Developers’ Association (Rehda) Institute serves as the industry’s knowledge hub and thought leadership platform, representing the collective voice, and developmental aspirations of Malaysia’s real estate stakeholders.

One of our primary roles is to build industry capacity and upskill the real estate stakeholders, ensuring that the Malaysian real estate market remains agile and informed amidst evolving market dynamics.

The Malaysian industrial economy

Over the last several decades, Malaysia’s industrial economy, covering manufacturing, mining and quarrying, and construction, has been a consistent growth engine. In 2024, it contributed approximately 37% of the national gross domestic product (GDP), with manufacturing alone making up an estimated 22%, second only to services at approximately 59%. This sustained economic strength has supported steady demand for factories, logistics facilities, and specialised industrial assets.

In recent years, demand has further accelerated because of the post-pandemic growth in e-commerce, rising foreign direct investment (FDI) in manufacturing, and the rapid expansion of data centres. At a time when the residential, office, and retail segments have faced greater uncertainty, the industrial property segment in the past few years have generally delivered stronger absorption, clearer yields, and growing interest from multinational occupiers, making industrial real estate an increasingly attractive segment for developers.

In the years following the Covid-19 pandemic, Rehda Institute’s market insights—through engagements with our members, and key stakeholders via our various forums, and surveys—highlighted a shift toward industrial real estate, with more developers exploring opportunities in this growing segment.

To support this transition, Rehda Institute introduced a series of Industrial Development Masterclasses and Market Insight Surveys beginning 2022, alongside very unique access to top industrial developments in Malaysia (i.e. Johor, Klang Valley, Penang) and also several overseas destinations (Singapore, Vietnam, Taiwan), through industrial study tours to award-winning industrial assets.

These platforms enabled meaningful engagement with authorities, industry experts, and practitioners, giving participants valuable insights into evolving market needs, regulatory trends, and sustainable industrial development practices. Building on these initiatives, Rehda Institute expanded its efforts this year by conducting a more comprehensive market insight survey among our developer members, and key industrial stakeholders. The findings, presented in this article, offer clearer insight into current market sentiment, opportunities, and challenges within Malaysia’s industrial real estate sector. This article aims to provide both an analytical snapshot and a strategic guide for developers navigating this rapidly evolving landscape.

What is powering the uptrend?

From our engagements, we believe that Malaysia’s industrial real estate growth is underpinned by several key drivers. First, continued capital expenditure, and supply-chain diversification by multinational corporations have brought strong FDI from China, Taiwan, the US, and other major markets, increasing demand for compliant, modern industrial facilities.

Second, national policy initiatives such as the National Energy Transition Roadmap (NETR), New Industrial Master Plan (NIMP) 2030, East Coast Rail Link (ECRL), and the Johor–Singapore Special Economic Zone (JS-SEZ) are enhancing connectivity, power reliability, and overall investor confidence across key industrial corridors. Third, the rapid expansion of e-commerce and data centres has driven demand for higher-spec warehouses and mission-critical infrastructure, resulting in stronger rental performance and faster take-up in strategic locations.

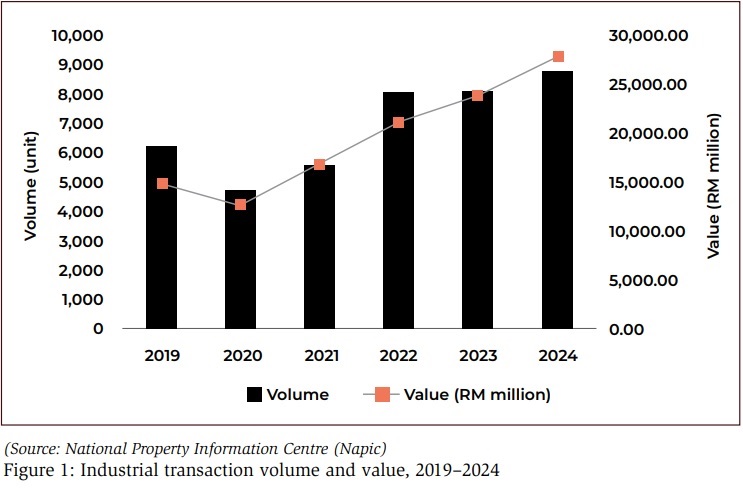

These forces show up clearly in the numbers: industrial transaction value and volume surged from RM12.76 billion (4,758 units) in 2020 to RM27.86 billion (8,783 units) in 2024, more than doubling value in four years (Figure 1).

.")

Beating the pack, despite a smaller base

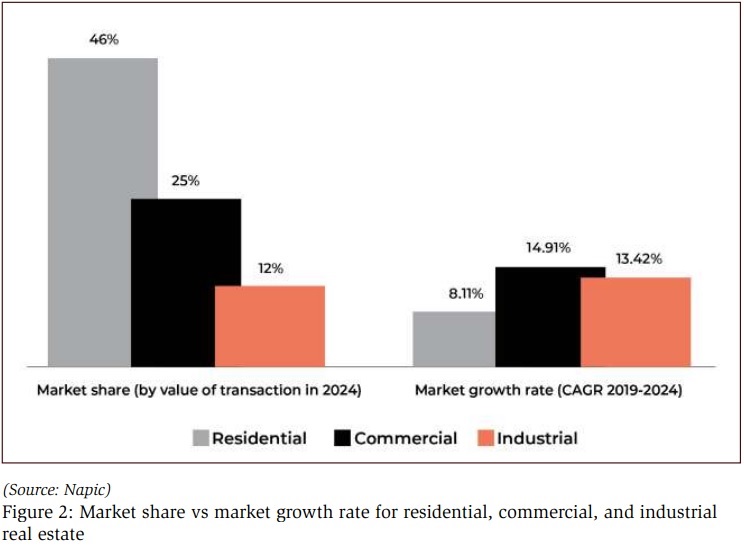

While industrial still represents a relatively modest, approximately 12% share (Figure 2) of total property transactions, its estimated 13.4% compound annual growth rate (CAGR) outstrips both residential, and commercial segments. Developers seem to increasingly prefer industrial for its stickier demand, lower leasing and management burden, and clearer yield profile, especially versus traditional offices and retail that face tech disruption, and versus residential, where costs, regulations, and sales cycles remain volatile.

Developer sentiment: upbeat, but selective

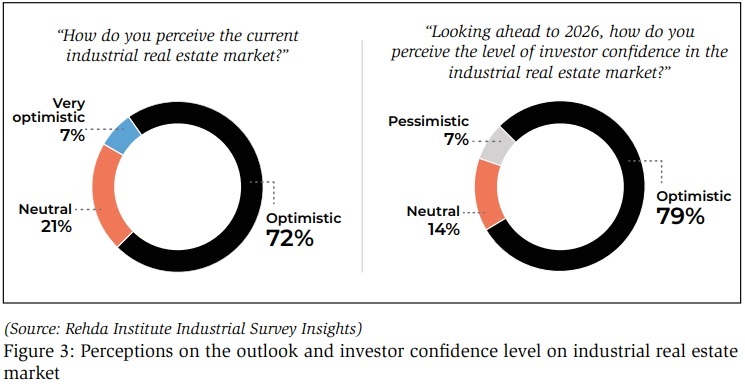

A recent Rehda Institute Industrial Survey Insights poll finds that around 79% of developers are optimistic about the industrial outlook, with most respondents also positive on investor confidence going forward (Figure 3).

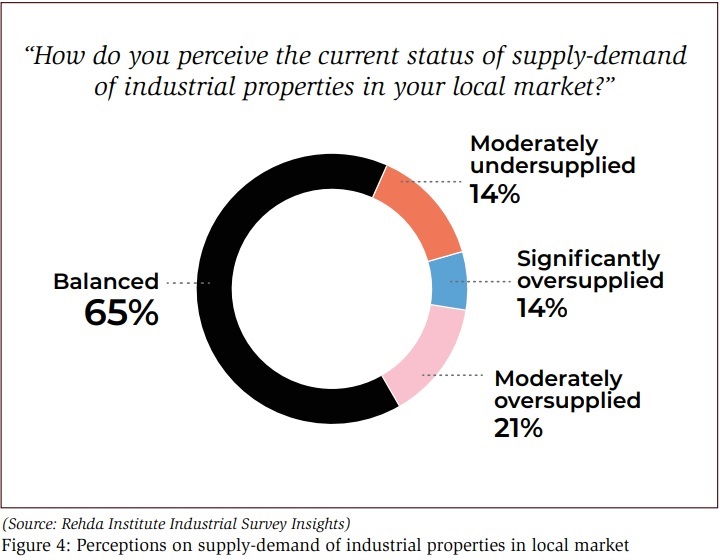

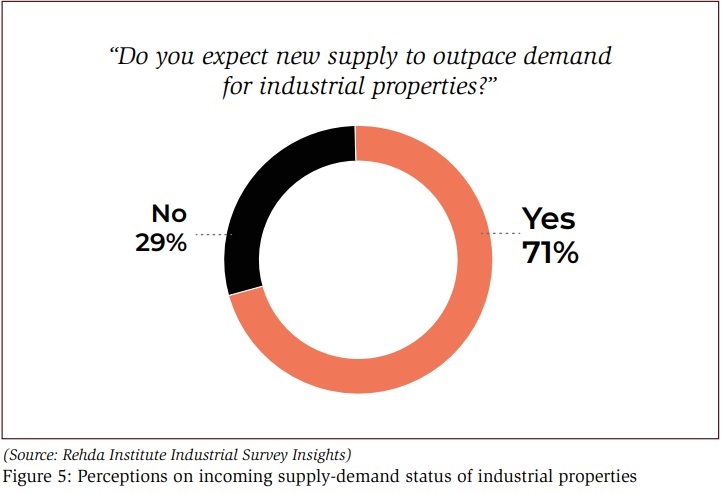

Yet, optimism is tempered by caution: an estimated 65% currently see balanced supply-demand (Figure 4), but an estimated 71% expect new supply to outpace demand in some localities if pipelines are not well-sequenced (Figure 5).

Where demand is most resilient:

Klang Valley, Johor, Penang: Logistics, e-commerce, and data-centre–adjacent assets continue to see healthy absorption, particularly where power, connectivity, and highways align.

Integrated industrial parks: Schemes that bundle utilities, high-spec roads, digital infrastructure, and shared services into a single, professionally-managed estate enjoy a leasing premium.

ESG: From tick-box to tenancy driver

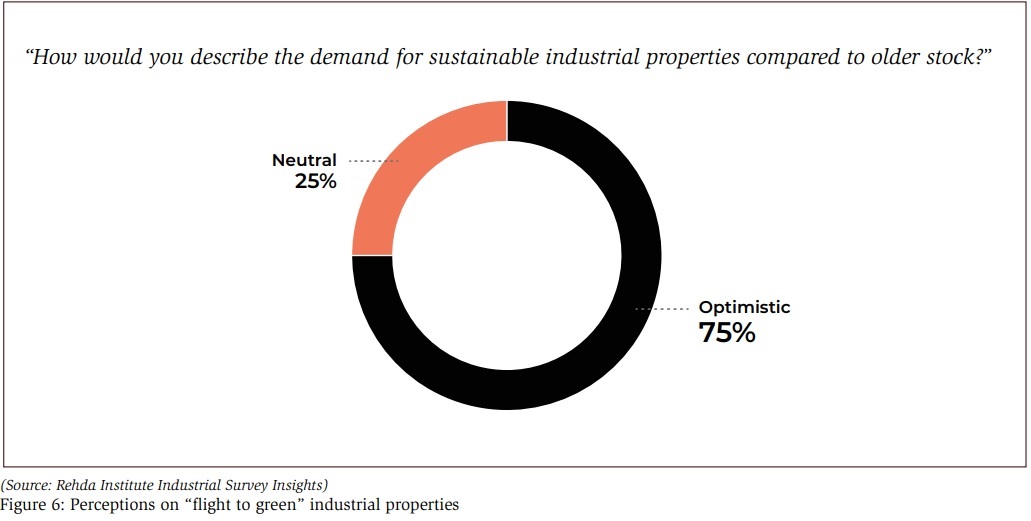

Developers report sharply rising tenant requirements around climate and compliance. Many multinational occupiers now align their facilities with corporate net-zero pathways and supply-chain reporting. Surveyed respondents overwhelmingly expect a “flight to green” (Figure 6): modern, efficient, and certifiable stock should outperform older inventory on rents, occupancy, and liquidity.

The risks: cost inflation, taxes, and oversupply

Beyond supply–demand imbalances, respondents flagged rising development and operating costs as top risks. Materials, and labour costs have escalated, and the expanded sales and service tax (SST) scope on commercial leasing, and construction services could compress margins further, raising the hurdle rate for new speculative projects, and potentially translating to higher rents or selling prices.

In high-spec segments like cold chain, powered plots, and data-centre shells, capital expenditure intensity makes careful phasing and pre-commitment vital.

Strategy playbook: how developers believe they can win (2026– 2028)

Curate location–infrastructure fit

Go where power capacity, grid resilience, and highway/port proximity converge.

JS-SEZ adjacencies, and ECRL-connected belts warrant a fresh look, but only with utility confirmation.

Build adaptable, future-proof specs

Design for multiple use-cases (light manufacturing to omnichannel logistics) with floor loading, clear heights, dock ratios, and yard depths that support diverse tenants.

Industrial park management as a product

Treat park governance, compliance support, and shared services as value-adds.

Operators that provide permit guidance; environment, health, and safety (EHS) playbooks, waste programmes, and digital tenant portals will command better retention and pricing.

Make ESG economical

Target payback-oriented green measures (lighting; heating, ventilation, and air conditioning (HVAC) optimisation, solar photovoltaics readiness, water reuse). Offer green-lease frameworks that align incentives, and simplify reporting.

Phase to demand, and protect yields

Where pipelines are heavy, go for smaller phases with pre-commit anchors. Manage exposure to cost escalations with indexed clauses and robust contingencies.

Bottom line

Malaysia’s industrial real estate is in a structural upcycle, but one that rewards discipline over exuberance. The winners will combine infrastructure-first site selection, ESG-ready design, and professional park management to deliver certainty and speed for occupiers.

For investors, the thesis remains compelling: growing demand, supportive policy, and rent-ready specifications, balanced by thoughtful phasing and cost control, should sustain attractive, risk-adjusted returns in the years ahead.

Summary

From our engagements and market insights, it illustrates that Malaysia’s industrial real estate sector stands at a defining moment. The data, developer insights, and ground realities captured in this report point to a market that is expanding rapidly but also one that is becoming more complex, competitive, and dependent on deeper technical expertise, stronger infrastructure planning, and clearer policy alignment.

As demand shifts towards higher-spec, ESG-aligned, and ecosystem-driven industrial environments, developers can no longer rely on traditional models.

We believe the future belongs to those who understand the evolving industrial landscape, and are ready to build smarter, more connected, and more resilient industrial ecosystems.

To support this transition, Rehda Institute will bring together senior developers, policymakers, and industry leaders at the Industrial Real Estate: Closed Door Strategic Dialogue & Masterclass, taking place on Nov 25 & 26, 2025 at Wisma Rehda, Kelana Jaya, Selangor.

The programme opens with a Closed Door Strategic Dialogue for developers to address bottlenecks, policy gaps, and emerging opportunities, followed by a full Industrial Development Masterclass featuring technical, policy, and market insights from leading experts.

Anchored by the findings of this report, the master class aims to help industry players navigate rising costs, ESG requirements, supply–demand shifts, and Malaysia’s accelerating industrial transformation, while fostering collaboration, alignment, and forward-looking strategies for the sector’s next phase.

As Malaysia accelerates towards a greener, smarter, and more globally-integrated industrial economy, the next phase will be shaped by those who act now, with clarity, collaboration, and conviction.

Allan Sim, Knight Frank Malaysia, senior executive director

The best opportunities for foreign investors are emerging in Malaysia’s high-tech and built-to-suit segments, where demand is outpacing existing supply. Penang’s Bayan Lepas and Batu Kawan remain the strongest magnets for semiconductor, electronics and precision-engineering investments, supported by deep supplier ecosystems and an engineering workforce unmatched elsewhere in the country.

Built-to-suit assets are gaining appeal across both Penang and Southern Johor, driven by manufacturers from China, Korea, Japan and the United States that require specialised facilities with high-spec floor loading, power infrastructure and automation compatibility. Johor’s SEZ framework with Singapore is reinforcing investor confidence, particularly for export manufacturing, logistics consolidation and data-centre infrastructure.

For investors seeking stable yields and scalable logistics platforms, Port Klang and Shah Alam remain the most liquid industrial locations in Malaysia.

These corridors offer modern warehouses, strong connectivity and a mature occupier base in FMCG, e-commerce and light manufacturing.

Emerging regions such as Negeri Sembilan and Kulim offer long-term upside for greenfield or campus-style developments at competitive entry costs.

(This interview response has been edited for brevity and clarity.)

FROM “PLOTS AND SHEDS” TO INTEGRATED ECOSYSTEMS

Survey feedback and engagements points to a clear evolution path:

Malaysia must move from fragmented, stand-alone “plots and sheds” to fully integrated industrial ecosystems that deliver:

*4IR (Industrial Revolution)-ready infrastructure: power quality, redundancy, and digital backbones that enable automation and real-time data • Environmental, social, and governance (ESG)-aligned hardware, and operations: energy efficiency, rooftop solar readiness, water stewardship, air quality, and waste systems incorporated from day one.

*People-supporting amenities: mobility, F&B, and dignified workforce accommodation (eg: centralised labour quarters) to improve productivity, and compliance standards This “industrial-as-a-service” approach blends hard infrastructure (power, water, information and communications technology (ICT), road geometry) with soft infrastructure (park management, compliance frameworks, digital permit systems) to give occupiers the speed, certainty, and reliability they need.

James Rix, JLL head of data centre and industrial, Malaysia and Indonesia

On data centre boom:

While data centres and AI factories are growing rapidly, their expansion has natural limits. The main constraints are power availability, and the global supply of chips that power graphics processing units (GPUs), along with the regulatory controls around them.

Power challenges can be eased through on-site generation, and alternative energy sources. Meanwhile, AI itself is here to stay, but current chip technologies still face supply restrictions.

In Malaysia, there is strong federal support for building an AI hub, with regulations being shaped to ensure growth remains within sensible guard rails. A clear sign that demand is real is American tech firm Nvidia is partnering with local data-centre operators, because where GPU manufacturers go, others will follow. Hyperscalers expanding in Malaysia also signal sustained interest in both AI and cloud infrastructure. Inference models will continue to grow as new uses emerge, while generative AI will expand through ongoing research.

Cloud remains essential, since many inference workloads still run there.

(This interview response has been edited for brevity and clarity.)

WHAT “GREEN” LOOKS LIKE IN PRACTICE:

*Efficient envelopes, and mechanical, electrical, and plumbing (MEP): better thermal performance, smart controls, and demand management

*On-site renewables, and storage readiness: wiring, roof loading, and interconnections planned from the outset

*Measurement and verification: data-driven-performance tracking is the new benchmark for transparency

POLICY PRIORITIES: CROWD IN CAPITAL, DE-RISK EXECUTION

Malaysia can amplify its competitive edge with a few targeted moves:

Grid, and permitting certainty: A clear power-allocation roadmap, faster substation approvals, and singlewindow facilitation for strategic parks will accelerate commitments.

Standardised ESG toolkits: Provide practical templates for monitoring and reporting to ease the burden on small and medium enterprises, and smaller developers.

Connectivity, and talent mobility: Invest in road/rail interfaces, inland container depots, and cross-border facilitation (especially around JSSEZ) to shorten logistics chains, and expand labour catchments.

Article and information compiled and written by Dr Foo Chee Hung, David S Chong, Pearljit Singh, and assisted by Syaidatul Akmal, and Dian Fazila

Disclaimer: This article has been compiled by Rehda Institute, drawing from insights gained through engagements with diverse industry stakeholders, its Market Insights Surveys, and feedback from Rehda Institute’s Industrial Masterclasses. While Rehda Institute has diligently worked to ensure the accuracy and reliability of the information presented herein, this content is intended solely for general informational purposes. It should not be considered professional advice or relied upon exclusively for making significant commercial decisions. Rehda Institute disclaims all liability for any loss or damage arising from reliance on the contents of this article, as the information reflects the opinions, sentiments, and perspectives gathered from a selection of our engaged stakeholders.

..........

Unlock Malaysia’s shifting industrial map. Track where new housing is emerging, as talents converge around Industry 4.0 parks across Peninsular Malaysia. Download the Industrial Special Report now.

{kind=link}